1.2 Taxonomy of Digital Assets

The four main types of digital money, their key differences, and why stablecoins offer a practical option for many everyday uses.

Disclaimer: Market figures reflect snapshots as of stated dates and change rapidly in digital asset markets.

Digital money comes in several forms, each designed to solve different problems. To understand stablecoins, we first need to see how they fit into the broader digital money landscape. Think of it like the difference between gold, dollars, and checks in the traditional world: each has its purpose, advantages, and limitations.

The digital money world has four main categories: cryptocurrencies (like digital gold), stablecoins (like digital dollars), central bank digital currencies or CBDCs (like digital cash issued by governments), and tokenized deposits (like digital checks from your bank). Let's explore what makes each unique and why stablecoins have emerged as the practical choice for everyday use.

Understanding the Four Types of Digital Money

To better understand where each type fits, consider the following visual spectrum based on volatility and use case.

Digital Asset Spectrum

Digital Asset Spectrum

1. Cryptocurrencies: Digital Gold

Bitcoin and Ethereum are the most well-known cryptocurrencies. Like gold, they're valuable because people agree they're valuable, not because any government or company guarantees their worth. Bitcoin has a fixed supply: only 21 million will ever exist, making it scarce like precious metals.

But here's the challenge: imagine trying to buy coffee with Bitcoin. By the time you finish drinking, your $5 coffee might have cost you $4 or $6. Bitcoin's value can swing dramatically. In 2021, it moved up or down by an average of 4% every single day 1. That's like the dollar losing or gaining the purchasing power of a gallon of milk daily. This volatility makes cryptocurrencies excellent for speculation but impractical for everyday use.

2. Stablecoins: Digital Dollars

Stablecoins solve the volatility problem by maintaining steady value, typically matching one US dollar. Think of them as digital versions of dollars that live on the same blockchain networks as Bitcoin and Ethereum but without the price roller coaster.

What makes stablecoins particularly powerful is their programmability. Unlike a traditional dollar transfer that simply moves from A to B, a stablecoin transfer can include conditions, automatic actions, and complex business logic. For example, a single stablecoin payment can be programmed to:

- Split automatically among multiple recipients based on preset percentages

- Hold in escrow until delivery is confirmed by GPS tracking

- Reverse automatically if certain conditions aren't met within a timeframe

- Generate instant loans using the payment as collateral

This transforms money from a static store of value into an active tool that can execute business processes automatically.

The $260 billion stablecoin market 2 uses three main approaches to maintain stability:

As of June 2025, the stablecoin market totaled approximately $260 billion 2, using three main approaches to maintain stability:

1. Fiat-backed (90% of market): Companies like Tether (USDT) and Circle (USDC) hold actual dollars and government bonds in bank accounts. For every digital token they issue, they keep one dollar in reserve. It's like a digital receipt for real money. Tether leads with $154 billion 3 while USDC holds about $47 billion 4. These companies publish regular attestations proving their reserves match tokens in circulation.

2. Crypto-backed: These use cryptocurrencies as collateral but require extra cushioning. Imagine putting down a $150,000 house as collateral for a $100,000 loan. That extra buffer protects against price drops. MakerDAO's DAI works this way, holding about $5 billion in various crypto assets to back its stablecoin. The over-collateralization means even if crypto prices fall 30%, each DAI still has backing worth $1.

3. Algorithmic: These attempted to maintain stability through automatic supply adjustments, like a thermostat for price. When demand increased, they'd create more tokens; when it decreased, they'd reduce supply. However, when Terra's UST collapsed in May 2022, $42 billion vanished in days 5, proving this approach remains experimental at best. Most users now avoid purely algorithmic stablecoins.

The programmability advantage becomes clear in practice. A business can create a smart contract that automatically:

- Pays suppliers only after receiving inventory confirmation

- Distributes revenue shares to partners based on performance metrics

- Manages escrow for real estate transactions without intermediaries

- Executes recurring payments with built-in conditions

This combination of stability and programmability explains why stablecoins have gained adoption for practical blockchain applications. You get the predictability needed for business operations plus the automation capabilities that traditional payment systems can't match.

3. Central Bank Digital Currencies (CBDCs): Government Digital Cash

CBDCs are digital currencies issued directly by central banks, essentially electronic versions of physical cash with full government backing. Unlike decentralized cryptocurrencies, CBDCs give governments complete control over monetary policy and transaction monitoring.

As of September 2024, 134 countries representing 98% of global GDP were exploring CBDCs 6, with 11 having launched digital currencies. However, adoption has been mixed: by the end of 2024, Nigeria's eNaira reached only 0.5% of the population despite heavy promotion 78, while China's digital yuan handles just 0.16% of domestic payments despite covering 260 million wallets as of June 2023 9. In Q1 2024, the European Central Bank has allocated €1.1 billion for its digital euro project 10, aiming to preserve monetary sovereignty while competing with private stablecoins.

4. Tokenized Deposits: Digital Bank Checks

The newest category, tokenized deposits, brings traditional banking onto blockchain rails. When JPMorgan created JPM Coin, they didn't invent a new currency. They simply made regular bank deposits moveable on blockchain networks. In June 2023, JPMorgan announced that JPM Coin was processing over $1 billion in daily transactions 11, operating exclusively between the bank's institutional clients.

Think of these as exclusive digital checks that only work within specific banking networks. Unlike stablecoins that anyone can use, tokenized deposits require bank relationships and operate under full banking regulations.

Comparing Stability: Why It Matters

The key difference between these digital assets is price stability. Here's a simple comparison:

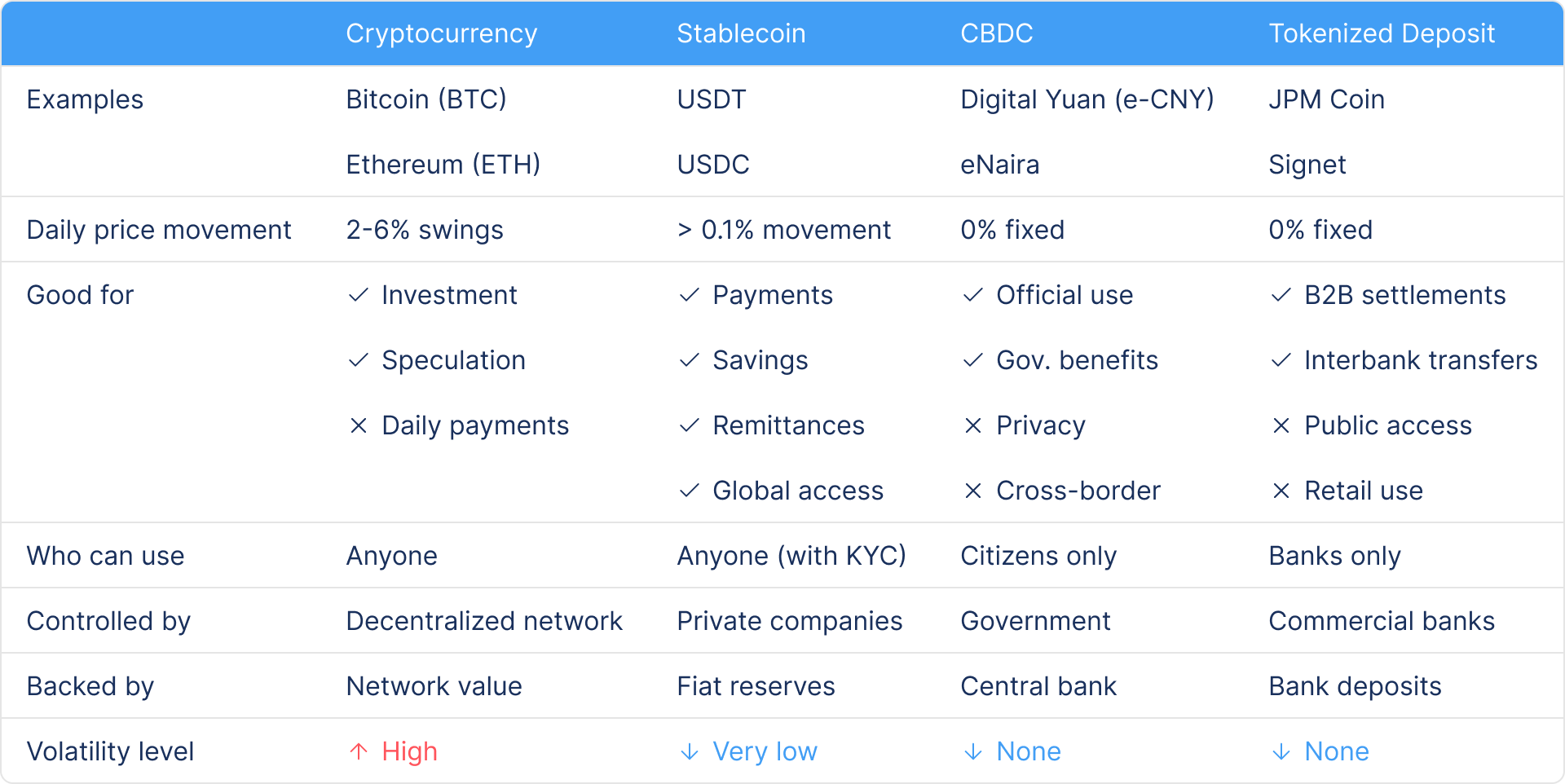

| Digital Asset Type | Daily Price Movement | Good For | Not Good For |

|---|---|---|---|

| Bitcoin | 2-5% typical swings | Long-term investment | Buying groceries |

| Ethereum | 3-6% typical swings | Running applications | Stable savings |

| Stablecoins | Less than 0.1% | Payments, savings | Investment growth |

| CBDCs | Zero (by design) | Government programs | Privacy needs |

| Tokenized Deposits | Zero (bank deposit) | Corporate settlements | Retail users |

This stability difference explains why stablecoins have become the preferred choice for practical applications. When you're sending money to family abroad, running a business, or saving for the future, you need money that holds its value between sending and receiving.

Making Sense of the Options

Each type of digital money serves different needs:

- Use cryptocurrencies when you want to invest or speculate on future value

- Use stablecoins when you need to make payments, save money, or transfer value quickly

- Use CBDCs when they become available for government services or official transactions

- Use tokenized deposits if you're a large corporation moving money between accounts

For most practical purposes, from remittances to business payments to inflation protection, stablecoins balance innovation with stability: the innovation of blockchain technology with the stability of traditional currency.

Among these digital asset categories, stablecoins have emerged as the practical bridge between volatile cryptocurrencies and traditional finance. But what exactly makes them "stable," and why does this stability matter so much for real-world adoption? The answer lies in understanding how they maintain their value and the problems this solves.

- Digital assets fall into four categories: cryptocurrencies (volatile investments), stablecoins (stable payments), CBDCs (government digital cash), and tokenized deposits (bank-only blockchain)

- Price stability is the critical difference: cryptocurrencies swing 2-6% daily while stablecoins maintain value within 0.1%

- Each type serves different needs: crypto for speculation, stablecoins for practical use, CBDCs for government control, tokenized deposits for banks

- Stablecoins hit the sweet spot by combining blockchain benefits with price stability, making them ideal for payments, savings, and remittances