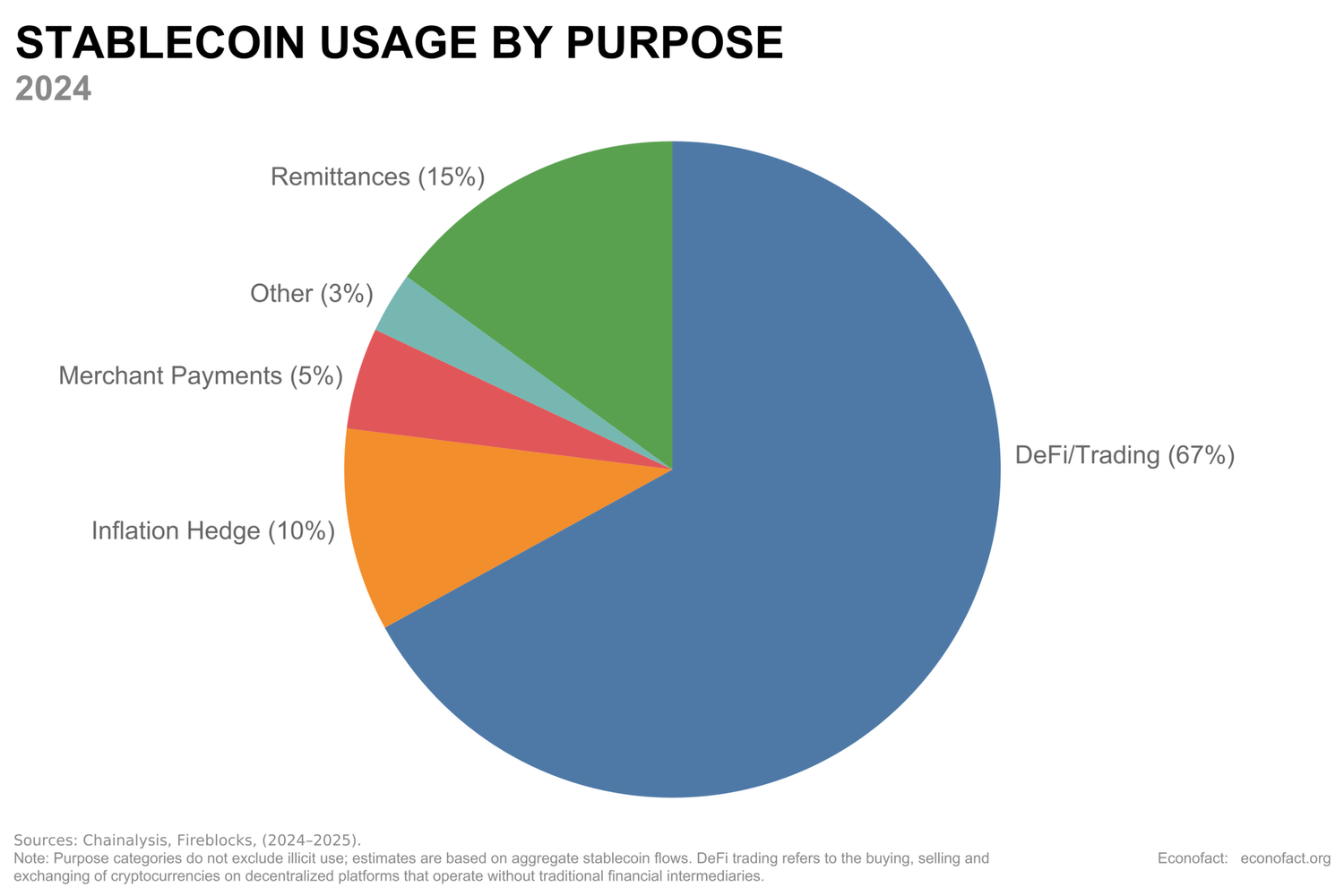

4.1 Retail Payments & Remittances

How stablecoins cut remittance costs by up to 85% compared to traditional services, and why adoption reached 30 million active wallets with 53% annual growth.

Every year, families across the developing world receive $685 billion in remittances from relatives working abroad 1. These transfers provide critical financial support for basic needs including food, housing, and education. Yet traditional money transfer services charge an average of 6.6% in fees 2, removing billions from recipients who can least afford these costs. Stablecoins now process $27.6 trillion in annual transfers 3, offering dramatic cost reductions and instant settlement that challenge centuries-old payment systems.

Source: ORF America

Source: ORF America

How remittances work today versus tomorrow

Traditional remittance systems involve multiple intermediaries. A Filipino nurse in Dubai sending money home navigates a complex chain: her bank, correspondent banks, exchange providers, and finally her family's local bank or cash pickup point. Each intermediary adds fees and processing time. The World Bank reports settlement times of 1-3 business days for 33% of transfers 2.

Stablecoin transfers eliminate most intermediaries. The same nurse uses a local exchange or crypto-enabled app to convert dirhams to USDC, sends it directly to her sister's mobile wallet in seconds, where a Philippine exchange like Coins.ph converts it to pesos. Total time: minutes. Total cost: 0.5-3% including all fees 4. Her sister receives 97 pesos for every 100 sent, not the 93 pesos traditional channels would deliver.

This efficiency explains rapid growth. The $2.3 trillion in "organic" stablecoin transactions (person-to-person transfers and merchant payments) grew 17% last year, while traditional remittances expanded just 2.3% 4. Stablecoins now reach tens of millions of active users globally 5, with adoption concentrated where traditional banking fails communities most.

Cost comparisons illustrate the advantage

The US-Mexico corridor demonstrates stablecoin advantages. A $100 remittance costs $1.99-8.49 through MoneyGram depending on speed, delivering $92.50-97.00 to recipients 6. The same transfer using Bitso with USDC on Stellar costs $1.25 total, and recipients get $98.75 in under one minute 7.

For a construction worker sending $500 monthly from Singapore to Bangladesh, traditional methods charging 6% mean $360 in annual fees. Stablecoin transfers at 1.5% save $270 yearly. That money buys three months of food or a child's school fees.

Speed matters beyond cost. Emergency medical funds arrive instantly, not days later. Families avoid dangerous trips to cash pickup locations. Money moves 24/7 regardless of banking hours or holidays.

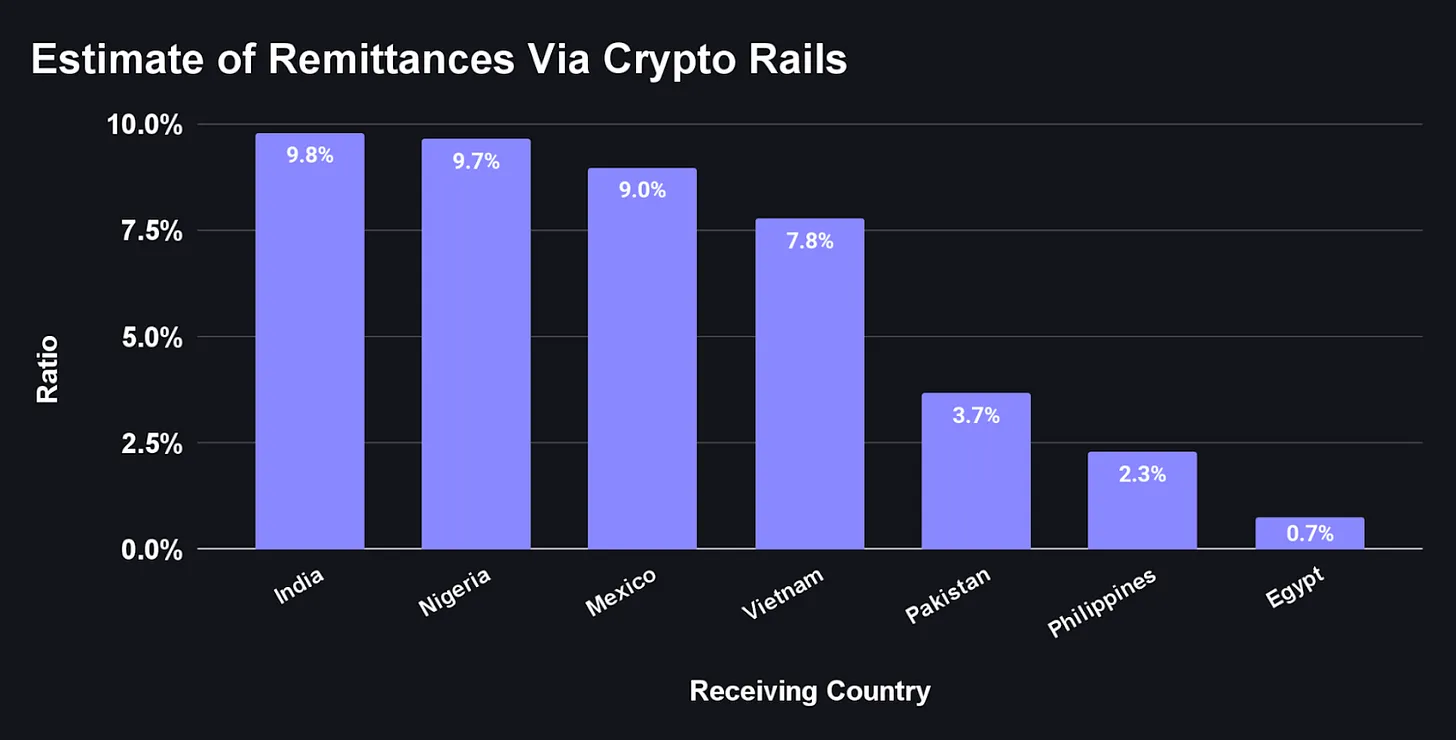

Regional adoption patterns

Top Receiving Remittance Countries Now 5-10% Via Stablecoins, Source: Artemis

Top Receiving Remittance Countries Now 5-10% Via Stablecoins, Source: Artemis

In Venezuela, 47% of transactions under $10,000 use stablecoins 8, the highest share in Latin America. Citizens cope with 172% inflation by immediately converting bolívars to USDT 9. Venezuelan residents processed $37.4 billion in crypto value annually, up 32% 8. Even small merchants accept stablecoin payments given frequent banking system disruptions and limited access to dollars.

Southeast Asia builds new financial infrastructure

The Philippines receives $38.34 billion annually from 2.16 million overseas workers, representing 8.3% of GDP 1011. Traditional corridors charge between 1.2% from Kuwait to 5.9% from Japan 12. The central bank's 2024 approval of PHPC (Philippine Peso Coin) represents an important milestone 13. This peso-backed stablecoin integrates with Coins.ph's 5 million users 14. Indonesia shows similar momentum, where 91% smartphone penetration provides the infrastructure needed for widespread digital wallet adoption. 15.

Africa circumvents systemic barriers

Nigeria ranks second globally in crypto adoption despite regulatory challenges 16. The naira's fall from ₦460 to ₦1,560+ since 2022 drives demand 17. With traditional channels imposing 30% spreads between official and parallel market rates 17, citizens moved $59 billion through crypto last year 16. Small businesses use USDT for imports when banks cannot provide dollars. Even government-launched cNGN struggles for adoption as users prefer established networks 18.

India leads by volume, lags in adoption

Despite receiving $111 billion in remittances annually—the world's largest—regulatory uncertainty limits stablecoin adoption to early adopters who save 4-5% on transfers. Pakistan ($30 billion) and Bangladesh ($22 billion) face similar dynamics. When regulations clarify, these markets could eclipse current volumes.

Payment infrastructure matures

Stablecoin payments have evolved from experimental use cases to everyday commerce infrastructure. BitPay connects users to 25,000+ merchants globally 19. Flexa enables spending at 41,000 locations including Nordstrom and Whole Foods 20. Strike's Lightning Network integration makes transfers nearly free for Latin American corridors 21.

E-commerce embraces the technology. Singapore merchants received $1 billion in crypto payments in Q2 2024 alone 22. Corporate adoption accelerates faster, with BVNK reporting average B2B transactions of $100,000-$250,000 23. Fireblocks processes 35+ million monthly transactions with 50% involving stablecoins 24.

Mobile integration has become necessary. GCash handles 17 million daily transactions across 3 million Philippine merchants 25. Both major Philippine wallets now support stablecoin services 26. Similar integration occurs across Indonesia's Dana, Thailand's TrueMoney, and Vietnam's MoMo.

These infrastructure developments create powerful network effects. Each merchant accepting stablecoins makes the system more useful for senders and recipients. A remittance recipient in Manila only benefits from receiving USDC if they can easily convert it to pesos at local exchanges or spend it directly at neighborhood stores. As more businesses integrate stablecoin payments and more exchanges offer conversion services, the value proposition strengthens for all participants. This creates a self-reinforcing cycle: more users attract more service providers, which attracts more users.

Barriers to mainstream adoption

Technical complexity excludes many potential users. Setting up wallets, managing private keys, and understanding blockchain transactions requires digital literacy many lack. The learning curve remains steep despite improved user interfaces. Chapter 5 provides step-by-step guidance for new users, including wallet setup, security practices, and executing first transactions.

Infrastructure gaps compound these challenges. Rural areas often lack reliable internet or smartphone access necessary for digital wallet usage. Without these basics, stablecoin adoption remains impossible regardless of cost advantages.

Regulatory confusion creates the largest obstacle. Some countries ban crypto entirely. Others allow trading but prohibit payments. Even supportive jurisdictions struggle with implementation. Users face different compliance requirements across platforms. Chapter 6 examines these regulatory frameworks in detail, including how regulations affect users, businesses, and the choice between regulated and unregulated options.

Infrastructure gaps persist outside major cities. Converting stablecoins to local currency requires exchanges or agents. Customer support rarely offers local languages. Scams targeting new users erode trust.

Price volatility during conversion windows can reduce expected value, though typically less than traditional fees. A 2% price movement during a 10-minute conversion still beats paying 6.6% in fees.

Traditional players respond to competitive pressure

Established remittance companies recognize the significant competitive pressure. MoneyGram partnered with Stellar for blockchain settlement. Western Union integrated Coinbase services. Competition already reduced traditional fees 33% over 15 years 4, but stablecoins accelerate this compression.

The UN's Sustainable Development Goal targets 3% average remittance costs by 2030 2. Stablecoins achieve this today through technology, not policy. As infrastructure improves and regulations stabilize, adoption will likely accelerate.

Traditional providers face decisions about technology integration as customer adoption accelerates. Stablecoin adoption reached over 30 million active wallets by early 2025, representing 53% growth from the previous year 5. This growing user base demonstrates that stablecoin remittances have moved from experimental use to established alternative.

- Traditional remittances average 6.6% in fees; stablecoins reduce this to 0.5-3% including all costs

- Venezuela leads with 47% of sub-$10,000 transactions using stablecoins; Philippines processes $38 billion in remittances annually

- Tens of millions of people use stablecoins globally, with adoption concentrated where traditional banking fails

- Technical complexity and regulatory confusion remain the largest barriers to mainstream adoption