5.1 Purpose and Functionality

What governance tokens actually control beyond voting, why real power over protocol parameters and multi-billion dollar treasuries creates value, and how free rider problems keep participation at 5-25% while the top 10 holders control 40-50% of any given protocol.

On March 12, 2020, Ethereum's price crashed 30% in hours. MakerDAO's collateral vaults liquidated rapidly. The system needed to mint 5.3 million new DAI to cover bad debt, but no central authority existed to make that decision. Instead, 80,000 MKR token holders voted. Within 48 hours, they passed an emergency proposal authorizing the debt auction. The system recovered without a CEO, board of directors, or emergency hotline to call 1.

This is what governance tokens do. They distribute decision-making power across token holders, replacing corporate hierarchies with on-chain voting systems.

The Traditional Problem

Every organization needs someone to make decisions. Who sets fees? Who upgrades software? Who allocates treasury funds? Who responds to emergencies?

Traditional companies answer with boards, executives, and voting shares. But blockchain protocols face a unique constraint: they're supposed to be decentralized. No single entity controls the code. No company owns the network. The community runs it collectively.

This creates genuine problems. Code needs updating. Parameters need adjusting. Treasuries need managing. Without governance mechanisms, protocols either stay static until they break or concentrate power in a development team's hands, destroying the decentralization they promised.

Early projects struggled with this tension. Some effectively gave developer teams permanent control, making "decentralization" more marketing than reality. Others committed to "code is law" and refused to add any upgrade mechanisms. This worked until critical bugs appeared and no mechanism existed to fix them. The DAO hack in 2016 demonstrated this failure spectacularly when $50 million in ETH got stolen and the community had no formal way to respond 2.

Governance tokens solve this by encoding voting rights directly into token economics. Hold the token, get voting power. Participate in proposals. Shape the protocol's future. No permission needed beyond owning the asset.

How Governance Tokens Create Decision Rights

Governance tokens are tokens with embedded voting rights. Many designs layer in economic rights like fee sharing or staking incentives, but the core function is coordinating collective decisions through token-weighted voting.

The technical implementation uses standard token contracts (typically ERC-20) combined with voting modules that count token holdings as vote weight.

Three components make this work:

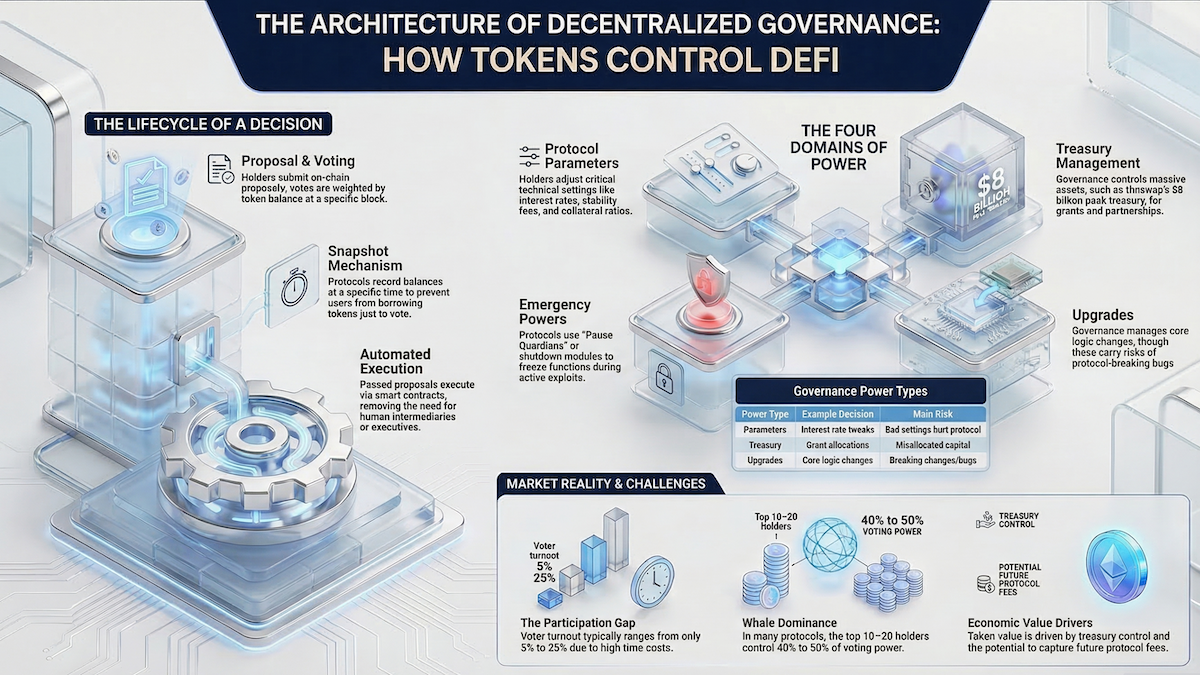

Proposal Creation: Token holders submit formal proposals describing specific changes. "Change the borrowing interest rate from 5% to 4.5%." "Allocate 100,000 tokens to marketing." "Upgrade the smart contract to version 2.0." These proposals exist on-chain as transactions with encoded parameters.

Voting Period: Token holders vote yes or no during a fixed window, usually 3-7 days. The protocol counts votes by checking token balances at a specific block (the "snapshot block"). This prevents people from borrowing tokens just to vote, then returning them immediately after.

Execution: If the proposal passes (usually requiring both minimum participation and majority support), the changes execute automatically through smart contracts. No intermediary implements the decision in mature designs. Passed proposals route through timelock contracts before execution, but humans can only propose changes, not manually enforce them. The code itself enforces the outcome.

This system differs from traditional corporate governance in one critical way: automation. Corporate shareholder votes often become advisory recommendations that management can ignore or delay. Protocol governance votes typically trigger immediate, irreversible changes to the live system. The code doesn't care about executive discretion or second thoughts.

Four Types of Governance Power

In practice, governance tokens usually control four domains: protocol parameters, treasuries, upgrades, and emergencies.

Not all governance tokens control the same things. The specific powers vary by protocol design.

Protocol Parameter Control

Most governance tokens start here. Token holders vote on technical parameters that control how the protocol operates.

MakerDAO's MKR holders vote on stability fees (interest rates for borrowing DAI), collateral types accepted in vaults, and liquidation penalties. When ETH price crashed in March 2020, MKR holders voted to increase the liquidation ratio from 150% to 170%, requiring borrowers to maintain higher collateral buffers 3. This single parameter change affected billions in locked value.

Compound's COMP holders set interest rate models, collateral factors, and which assets the protocol accepts. In 2021, they voted to add AAVE as collateral despite AAVE being a direct competitor 4. Traditional companies rarely let shareholders decide to support competitors.

Uniswap's UNI holders control protocol fees. The default is 0% (making it free to trade), but governance can enable a 0.05% protocol fee on any trading pair, diverting revenue from liquidity providers to the protocol treasury 5. This remains off because LPs oppose reducing their share, demonstrating how tokenized voting creates real checks on protocol extraction.

Treasury Management

Many protocols accumulate tokens, fees, or other assets in community treasuries. Governance tokens control how these funds get spent.

Uniswap's treasury held 1 billion UNI at launch (roughly $8 billion at peak) plus accumulated trading fees 6. Token holders vote on grants, partnerships, and investments. They funded $1.8 million to Stanford University for blockchain research and $3 million to Polygon to incentivize Uniswap v3 adoption on that chain 7. Compound and Optimism follow similar patterns, with governance controlling $150+ million and $1+ billion in treasury assets respectively 89.

This treasury control matters because it determines whether protocols act like decentralized public goods or extractive businesses. Traditional venture-backed companies prioritize investor returns. DAOs can prioritize community benefit, ecosystem growth, or long-term sustainability instead. The token holders decide.

Smart Contract Upgrades

Most DeFi protocols use upgradeable smart contracts, where governance can modify the core code. This creates real power but also introduces risk.

Compound v2 lets COMP holders vote on new market listings, interest rate changes, and collateral factors. But they cannot modify the core lending logic without deploying entirely new contracts. This limits governance scope to parameters, not basic mechanics.

MakerDAO takes a different approach. MKR holders vote on "executive proposals" that can modify nearly anything about the protocol, including the core CDP (Collateralized Debt Position) engine that creates DAI. This gives more flexibility but concentrates more power. A compromised governance process could break the system completely.

Aave implemented a middle ground with a tiered upgrade system. Minor changes (like interest rate tweaks) require standard governance votes. Major changes (like new markets or protocol architecture) require both governance approval and a mandatory time delay before execution 10. This delay gives users time to exit if they disagree with the direction.

The technical mechanism works through proxy contracts. Users interact with a proxy that delegates calls to an implementation contract. Governance votes can point the proxy to new implementation contracts, effectively upgrading the system without changing the user-facing addresses.

Emergency Powers

Ironically, many governance tokens include mechanisms to bypass normal governance during emergencies. This contradicts decentralization in theory but prevents catastrophic failures in practice.

Compound has a "pause guardian" that can immediately freeze specific protocol functions if an exploit is detected 11. This guardian is controlled by a multisig wallet held by the Compound Labs team, not by governance. The community accepted this trade-off because 7-day voting periods can't respond to active exploits draining millions per hour.

MakerDAO's Emergency Shutdown Module allows MKR holders to trigger a complete protocol shutdown, freezing all CDPs and letting users withdraw collateral 12. This exists specifically for black swan events where the system becomes insolvent. It's never been used in production but prevented total loss scenarios in multiple near-misses.

Aave's guardian can pause borrowing, lending, or liquidations per market 13. When Curve's CRV token got exploited in 2023, Aave's guardian immediately paused CRV borrowing to prevent the exploit from cascading into Aave's markets 14. Governance ratified this action after the fact.

These emergency powers reveal the tension in governance token design. Pure decentralization means no one can act quickly. But "no one can act quickly" includes responding to attacks, bugs, or market manipulation. Most successful protocols choose pragmatic hybrid models: decentralized for normal operations, centralized for emergencies, with clear limits on emergency powers.

Summary: Governance Power Types

| Power Type | Example Decision | Main Risk | Example Protocol |

|---|---|---|---|

| Protocol Parameters | Interest rate adjustments | Bad parameters hurt protocol | MakerDAO, Compound |

| Treasury Management | Grant allocations | Misallocated capital | Uniswap, Optimism |

| Smart Contract Upgrades | Core logic changes | Breaking changes | Aave, MakerDAO |

| Emergency Powers | Pause functions during exploits | Centralization risk | Compound, Aave |

Why Governance Tokens Have Value

A token that only grants voting rights seems worthless. You can't spend it. It pays no dividends. It produces nothing physical. Yet MKR trades at $1,400+, COMP at $50+, UNI at $6+ as of late 2024.

Before looking at the practical scope of that power, it helps to understand why markets price these tokens at all.

Three factors create this value:

Control Over Future Cash Flows

Protocols generate revenue through fees. Uniswap charges 0.3% on every trade. Aave charges interest on loans. MakerDAO charges stability fees on borrowed DAI.

Currently, most protocols direct these fees to liquidity providers or burn tokens. But governance could vote to capture fees for token holders instead. Uniswap's governance controls a "protocol fee switch" that could divert 0.05% of trading fees to UNI holders 5. This represents billions in potential annual revenue. UNI's value partially reflects the option to activate this switch.

MKR holders already capture value directly. When MakerDAO burns MKR tokens using protocol revenue, the remaining supply becomes scarcer. The protocol has burned over 40,000 MKR (worth $50+ million) 15. Each burn increases remaining holders' percentage ownership of future governance and fees.

Control Over Valuable Treasuries

Governance tokens control protocol treasuries. Uniswap's treasury held $8 billion at peak. Optimism's treasury distributed $1+ billion in OP tokens through governance votes 9. These assets belong to token holders collectively.

Traditional corporations have enterprise value based partly on assets minus liabilities. DAOs' treasuries work similarly. If Uniswap governance decided to liquidate the protocol and distribute all treasury assets proportionally to UNI holders, each token would claim its share. This creates a lower bound on rational token valuation, though most tokens trade well above this liquidation value because future control exceeds current assets.

Market Pricing of Governance Influence

Some entities want voting power for strategic reasons beyond financial return. Competitors might buy governance tokens to influence parameters that favor their products. Service providers might accumulate tokens to secure ongoing contracts. Large users might hold tokens to protect against hostile governance changes.

This creates demand unrelated to cash flows or treasury value. The token becomes a strategic asset for influencing a major protocol's direction. When Compound listed AAVE as collateral, AAVE holders benefited operationally 4. Both communities had incentives to hold each other's governance tokens to maintain friendly relations.

The Free Rider Problem

Governance tokens face a paradox. Voting determines the protocol's value, but voting costs time and attention. Most holders don't vote.

Uniswap's governance proposals typically see 5-10% participation rates 16. Compound averages 8-15% 17. MakerDAO achieves higher rates (15-25%) but still represents a minority of token holders 18.

This happens because voting is expensive in time, not just gas fees. Reading proposals requires understanding technical parameters and evaluating economic trade-offs. Informed voting can cost hours per proposal.

But whether you vote or not, you benefit or suffer from governance outcomes equally. Buy 100 MKR tokens and never vote, you still gain when the protocol succeeds. Rational actors free ride, letting others do the work while capturing the benefits.

Two mechanisms partially address this:

Delegation: Token holders can delegate voting power to addresses they trust without transferring tokens. Uniswap and Compound both support this 19. You keep economic ownership but outsource governance participation to community members who specialize in protocol evaluation. This concentrates power in visible delegates at the cost of centralization risk. Uniswap's delegation system partially addresses the free rider problem by concentrating power in accountable delegates, though it trades one problem (apathy) for another (centralization).

Vote Incentives: Curve pioneered paying voters to participate through its veCRV (vote-escrowed CRV) system 20. Token holders who lock tokens and vote regularly earn boosted rewards. This aligns governance participation with economic benefit, though it also increases whale concentration since large holders earn more from these incentives.

These solutions help but don't eliminate the problem. Most token holders still don't vote.

The Whale Problem

Governance tokens typically follow one-token-one-vote. Hold more tokens, get more votes. This creates plutocracy by design.

Compound's top 10 addresses control over 40% of voting power 21. Uniswap's top 20 control 50%+ 22. These whales can pass or block proposals unilaterally.

The concentration happens naturally. Early investors, founders, and core teams receive large token allocations. Market dynamics create inequality that governance enshrines.

Two approaches attempt to mitigate this:

Time-Based Weight: Curve's veCRV gives more voting power the longer you lock tokens 20. Lock for 4 years, get 100% vote weight. Lock for 1 year, get 25%. This biases governance toward long-term holders with stronger protocol alignment. The mechanism doesn't prevent whales from dominating, but it ensures those whales have committed capital they can't easily exit.

Quadratic Voting: Vote weight scales by square root of tokens held. 100 tokens give you 10 votes. 10,000 tokens give you 100 votes. This dampens whale power but creates sybil attack vulnerabilities where whales split holdings across multiple addresses 23. Gitcoin uses quadratic voting for grants but requires identity verification, which conflicts with crypto's pseudonymous ethos.

| Mechanism | How It Works | Effect on Whale Power | Main Vulnerability | Used By |

|---|---|---|---|---|

| Standard (1-token-1-vote) | Token balance at snapshot block = vote weight | None — concentration is encoded directly | Whales pass or block proposals unilaterally | Compound, Uniswap |

| Time-locked weight (veCRV) | Longer lock = higher vote weight (4 years = 100%, 1 year = 25%) | Partial — large holders still dominate, but must commit capital they can't exit quickly | Whales lock large positions for maximum weight; long lockups reduce liquidity | Curve, Aave |

| Quadratic voting | Vote weight = √(tokens held): 100 tokens → 10 votes, 10,000 tokens → 100 votes | Meaningful — compresses the gap between small and large holders | Sybil attacks: whales split holdings across many wallets to reset the curve | Gitcoin (with identity verification) |

Neither solution works perfectly. Whales still dominate most protocol governance. The industry largely accepts this as inevitable since tokens represent economic stake, and those with the most at risk arguably should control decisions.

What Governance Tokens Actually Govern

These value drivers explain why markets price governance tokens. But that pricing depends on what token holders actually control. The scope of governance power varies dramatically across protocols.

The name "governance token" suggests complete control. The reality is more limited.

Many protocols put only specific functions under governance while keeping core mechanics immutable or controlled by developer teams. This hybrid approach balances decentralization ideals with practical realities.

Uniswap's governance cannot change the core AMM (Automated Market Maker) mathematics 24. The x*y=k formula that defines liquidity pools is hardcoded and immutable. Governance controls fees, treasury spending, and new market deployments, but it cannot alter the basic trading mechanics without deploying entirely new contracts and migrating liquidity.

USDC's governance model is even more restricted. Circle controls the smart contract completely 25. Governance tokens don't exist. The company can freeze accounts, blacklist addresses, and upgrade contracts unilaterally. Users choose to trust Circle's centralized governance based on regulatory compliance and business reputation, not on-chain voting.

This raises a question: when does "governance token" become a misnomer? If token holders control only minor parameters while a company controls the core protocol, is it really governed by tokens? The marketing says yes. The smart contracts often say no.

The best governance tokens control meaningful decisions with real economic impact while preserving the protocol's core value proposition. MakerDAO's MKR fits this pattern. MKR holders control parameters that determine DAI's stability, but they cannot simply vote to steal user collateral or break the basic CDP mechanics. The governance scope is broad but not unlimited.

From Theory to Practice

Governance tokens transformed crypto from a technical experiment into an economic coordination mechanism. They let protocols operate without companies while maintaining the ability to adapt and improve.

The execution remains messy. Low participation, whale dominance, and limited scopes all constrain effectiveness. But the alternative is worse: either protocols stay rigid until they break or they centralize control and lose the decentralization they promised.

The next section examines voting mechanisms and DAO integration, covering the technical implementation details that transform abstract governance rights into operational protocol control. But first, let's see what happens when those mechanisms face real-world pressure.

- MKR holders replaced an emergency board meeting with an on-chain vote, covering $5.3 million in bad debt within 48 hours of the 2020 crash.

- Uniswap's treasury held $8 billion at peak. Token holders vote on every grant and investment, including $1.8 million to Stanford for blockchain research.

- Governance participation averages 5-25% across major protocols, meaning a minority makes decisions for the majority while most holders free-ride on the outcomes.

- Compound's top 10 addresses hold 45% of voting power. Uniswap's top 20 hold over 50%. Token-weighted governance doesn't fight plutocracy, it encodes it.

- Uniswap's governance controls fees, treasury, and new markets but cannot modify the core trading formula. "Governance token" doesn't mean holders control what matters most.