8.1 Types of Stability Mechanisms

How different stablecoin designs maintain a $1 peg without central banks, the fundamental trade-offs each approach makes, and why some mechanisms dominate the market while others spectacularly fail.

Building a digital asset that holds exactly $1 of value presents an engineering problem unlike anything in traditional finance. The blockchain has no Federal Reserve to adjust interest rates, no FDIC to insure deposits, no lender of last resort to provide emergency liquidity. Yet billions of dollars in stablecoins trade hands every second, maintaining their peg through mechanisms that range from straightforward to extraordinarily complex.

The challenge boils down to this: how do you anchor digital tokens to real-world value when everything happens in a decentralized environment designed to eliminate trusted intermediaries?

Every design decision in stablecoin architecture flows from how a project answers that fundamental question. The choices made determine everything: who can freeze your funds, what happens during market crashes, how much capital gets tied up supporting each dollar of stablecoins, and whether the system can survive without centralized control.

In May 2022, TerraUSD demonstrated what happens when those choices go catastrophically wrong. This algorithmic stablecoin promised to maintain its peg through automated supply adjustments rather than reserves. For months it worked, growing to $18 billion in circulation and becoming one of the largest stablecoins in the market. Then, in just 72 hours, it collapsed to near zero. The destruction rippled across the entire Terra ecosystem, wiping out $60 billion in total value. Thousands lost life savings. The event sent shockwaves through crypto markets and forced everyone to confront an uncomfortable truth: some stability mechanisms work under normal conditions but break catastrophically under stress 1.

Understanding why Terra failed while USDC survived requires examining the fundamental trade-offs encoded into every stablecoin design. These trade-offs aren't minor technical details. They determine whether a stablecoin can actually deliver on its promise when users need it most.

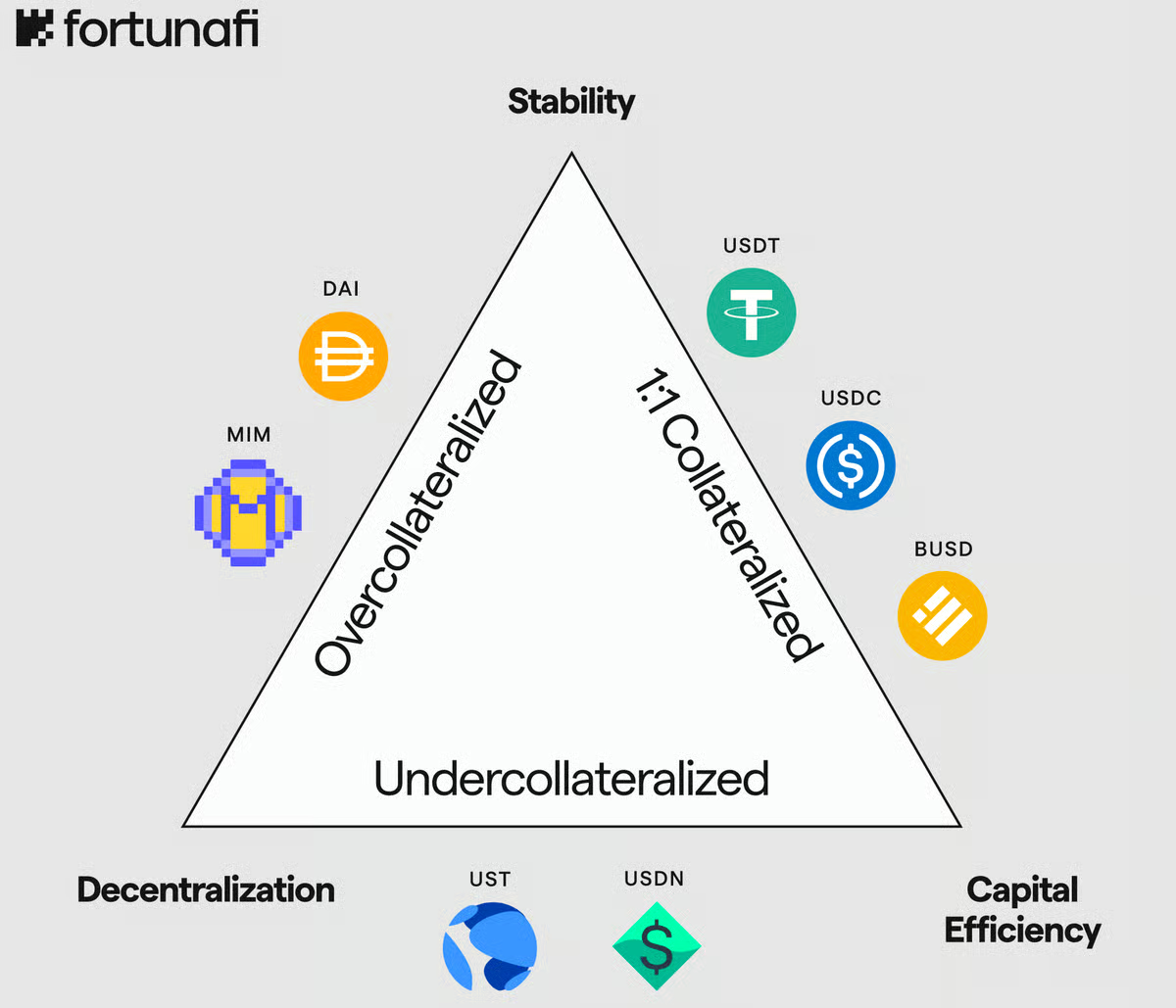

The Stablecoin Trilemma

The concept of the Stablecoin Trilemma, adapted from the impossible trinity in traditional monetary economics, provides the clearest framework for understanding these design constraints 2. Every stablecoin aims for three desirable properties, but achieving all three simultaneously proves impossible with current designs.

Price Stability: The Core Promise

A stablecoin must maintain its peg to the dollar. This isn't optional. If 1 USDC trades at $0.92 one day and $1.07 the next, it fails its purpose. Users need predictable value for payments, trading, and storing wealth. Perfect stability would mean 1 token equals exactly $1.00000 at every moment, regardless of market conditions.

Real-world stability is messier. USDC typically trades between $0.9999 and $1.0001. DAI fluctuates slightly more, sometimes reaching $1.02 or $0.98 during volatile periods. These small deviations are acceptable. Sustained breaks below $0.95 or above $1.05 signal serious problems.

The March 2023 Silicon Valley Bank collapse tested this property directly. When Circle disclosed $3.3 billion trapped in the failed bank, USDC plunged to $0.87 as panic spread. The peg recovered within 72 hours after the Federal Reserve guaranteed deposits, but those 72 hours revealed how quickly confidence can evaporate 3.

Capital Efficiency: The Economic Constraint

Capital efficiency measures how much collateral you must lock up to create $1 of stablecoins. This matters enormously for scalability and cost.

Fiat-backed stablecoins achieve 1:1 efficiency. Circle holds one dollar for every USDC in circulation. Maximum efficiency, zero waste.

Crypto-backed stablecoins require over-collateralization. MakerDAO demands $150-200 of ETH to generate $100 of DAI. This 150-200% collateralization ratio protects against crypto volatility. When ETH drops 30%, the system maintains backing. But it means $8 billion locked in MakerDAO vaults only produces $5 billion in DAI. That $3 billion difference represents capital that could be deployed elsewhere.

Algorithmic designs theoretically achieve infinite efficiency. No collateral needed, just code managing supply. Terra's UST exemplified this approach. The promise of capital-free stablecoins looked revolutionary until the system collapsed, proving efficiency means nothing without stability.

Decentralization: The Control Question

Decentralization determines who controls the system and whether anyone can freeze your funds.

Fully decentralized stablecoins operate through transparent smart contracts without human intervention. Anyone can verify the code. No company can blacklist addresses. No government can shut down operations. DAI represents this model: MakerDAO's smart contracts execute automatically, with governance decisions made by MKR token holders rather than a company board.

Centralized stablecoins vest control in specific companies. Circle can freeze USDC addresses, block transactions, and control minting through administrative keys. This centralization enables regulatory compliance and institutional trust. When law enforcement requests it, Circle complies. When governments demand transparency, Circle provides audits. This control proved valuable for adoption but contradicts cryptocurrency's original promise of financial sovereignty.

The trilemma states you can optimize for two properties but rarely achieve all three. This constraint shapes every major stablecoin design:

- High Stability + High Efficiency = Low Decentralization (USDC, USDT): Real dollars back each token with perfect efficiency, but companies control everything

- High Stability + High Decentralization = Low Efficiency (DAI): Over-collateralization and automated mechanisms maintain stability without central control, but capital efficiency suffers

- High Decentralization + High Efficiency = Low Stability (UST, failed): Algorithmic mechanisms promised both benefits but couldn't maintain the peg under pressure

The Stablecoin Trilemma. Source: Fortunafi

The Stablecoin Trilemma. Source: Fortunafi

Understanding this framework explains why certain designs dominate the market. USDT and USDC account for over 90% of stablecoin market share because most users prioritize stability above all else. They accept centralization as the price for reliability. Crypto-native users gravitate toward DAI despite lower capital efficiency because decentralization matters more to them than optimal capital use. Algorithmic experiments continue attracting builders despite Terra's failure because the theoretical benefits of solving the trilemma remain compelling.

The Four Stability Mechanism Families

Stablecoins maintain their pegs through four broad mechanism families. Each family takes a different approach to the engineering challenge, making different trade-offs across the trilemma.

Fiat-Collateralized: Real Dollars Hold the Peg

This is the simplest and most successful model. For every token in circulation, the issuer holds one dollar or dollar-equivalent assets in regulated financial institutions.

Tether issues USDT backed by dollars, Treasury bills, and other cash equivalents held in bank accounts 4. Circle issues USDC backed exclusively by cash and short-term U.S. Treasuries 5. The mechanism is straightforward: users deposit dollars, receive tokens. Users return tokens, receive dollars. The issuer maintains 1:1 backing at all times.

The smart contract mechanics, as detailed in [[2.2 Smart Contracts and Token Creation]], handle the blockchain side. Circle deploys ERC-20 contracts that manage minting and burning. When someone deposits $1 million, Circle mints 1 million new USDC tokens to that address. When someone redeems 1 million USDC, Circle burns those tokens and transfers $1 million from reserves.

This model dominates because it works reliably. USDT has processed over $120 trillion in cumulative transaction volume since 2014 6. USDC serves as the primary dollar gateway for institutional crypto adoption. The stability record speaks for itself.

The trade-offs are clear: perfect stability and efficiency, but complete centralization. Circle controls USDC entirely. Tether controls USDT entirely. Users trust these companies to maintain reserves, honor redemptions, and comply with regulatory requirements.

Crypto-Collateralized: Over-Collateralized On-Chain Assets

This model uses other cryptocurrencies as backing while maintaining operations through smart contracts rather than companies.

MakerDAO created the standard approach with DAI. Users deposit ETH, WBTC, or other approved crypto assets into smart contracts called Vaults. The protocol allows them to generate DAI against this collateral, but never at 1:1. Typical collateralization ratios range from 150% to 200%. Deposit $1,500 of ETH, generate up to $1,000 of DAI.

This over-collateralization protects the peg during volatility. If ETH drops 20%, that $1,500 becomes $1,200. The system remains solvent because it only created $1,000 in DAI. If ETH continues dropping and collateral falls below 150% of the DAI debt, the system automatically liquidates the position. It auctions the ETH for DAI to close the debt, adds a 13% penalty fee, and maintains systemic backing 7.

Price oracles enable this automation. The smart contracts must know ETH's current value to calculate collateralization ratios and trigger liquidations. Chainlink and other oracle networks provide these price feeds. The March 2020 "Black Thursday" event tested this mechanism when ETH dropped 50% in 24 hours. Some liquidations executed imperfectly due to network congestion, but DAI maintained its peg and the system survived 8.

The trade-offs here flip: high stability through over-collateralization, high decentralization through autonomous smart contracts, but terrible capital efficiency. Billions sit locked in Vaults that could otherwise be deployed productively.

Algorithmic: Supply-and-Demand Software Mechanics

Algorithmic stablecoins attempt to maintain stability through automated supply adjustments without any backing assets. The promise is compelling: achieve stability through pure mechanism design, no collateral required.

The theory works like this: when demand increases and price rises above $1, mint new tokens to increase supply and push price down. When demand decreases and price falls below $1, reduce supply to push price back up. Implement this through incentive mechanisms that encourage traders to arbitrage deviations back to peg.

Terra's UST used a two-token model. UST was the stablecoin. LUNA was the volatile collateral token. Users could always burn $1 of LUNA to mint 1 UST, or burn 1 UST to mint $1 of LUNA. This arbitrage mechanism theoretically maintained the peg:

- UST trades at $1.05: Burn $1 LUNA, mint 1 UST, sell for $1.05, pocket $0.05 profit. Repeated arbitrage increases UST supply until price returns to $1.

- UST trades at $0.95: Buy 1 UST for $0.95, burn it to mint $1 LUNA, sell LUNA for $1, pocket $0.05 profit. Repeated arbitrage decreases UST supply until price returns to $1.

The fatal flaw became obvious in May 2022. Large UST redemptions triggered LUNA minting to absorb the supply. LUNA's price crashed as billions of new tokens flooded the market. This crash reduced LUNA's value, requiring even more LUNA minting to back each UST. The death spiral accelerated: falling LUNA prices required more minting, which caused more falling. Within days, LUNA went from $80 to $0.00001. UST's peg shattered permanently 9.

The mechanism failed because it relied on confidence rather than assets. Fiat-backed stablecoins have dollars. Crypto-backed stablecoins have over-collateralized assets. Algorithmic stablecoins have only belief that the mechanism will work. Once belief breaks, nothing stops the collapse.

Multiple algorithmic designs have failed catastrophically: Basis Cash, Empty Set Dollar, Iron Finance, and most dramatically Terra. Each promised to solve the trilemma through clever mechanism design. Each discovered that mechanism design alone cannot create stable value.

The trade-offs: theoretical perfect efficiency and decentralization, but stability that evaporates under stress.

Hybrid and Emerging Models: Delta-Neutral Synthetics and Yield-Bearing Treasury-Backed Designs

Terra's collapse didn't end innovation. It refocused attention on more sophisticated hybrid approaches.

Delta-Neutral Synthetic Dollars: Ethena's USDe demonstrates a new model that has scaled to over $14 billion in circulation. This approach maintains stability through balanced positions rather than pure collateral 10.

The mechanism works like this: Hold $1 of ETH. Simultaneously open a $1 short position in ETH perpetual futures. If ETH rises 10%, the spot position gains $0.10 but the short loses $0.10. If ETH falls 10%, the spot loses $0.10 but the short gains $0.10. Net position stays exactly $1 regardless of price movement.

This delta-neutral strategy maintains stable value without over-collateralization. The capital efficiency matches fiat-backed models. Decentralization is partial: positions are transparent on-chain but depend on derivatives exchanges as counterparties.

The bonus comes from funding rates. Perpetual futures typically trade at premiums during bull markets. Traders pay funding to maintain long positions. The delta-neutral strategy collects this funding as yield, often 5-15% annually. Unlike fiat-backed stablecoins where issuers keep reserve yields, USDe shares returns with holders.

The October 2025 launch of suiUSDe on the Sui blockchain extended this model beyond Ethereum, proving the mechanism works across different networks 11.

The risks are real: funding rates can turn negative during bear markets, costing money instead of earning it. Exchange failures create counterparty risk. The complexity far exceeds simple collateral backing. But the model offers an interesting middle path through the trilemma.

U.S. Treasury-Backed Yield-Bearing Stablecoins: Ondo's USDY and Hashnote's USYC take fiat backing in a new direction. Instead of generic dollar reserves, they hold specifically U.S. Treasury bills and pass interest to token holders 12.

Traditional fiat-backed stablecoins generate significant profits from their reserves. Circle earns roughly 5% annually on the $50+ billion backing USDC. That's $2.5+ billion in annual profit that token holders never see. Yield-bearing models distribute this income to users.

The mechanism maintains 1:1 backing with Treasuries while distributing interest. Users hold stable $1 value plus earn 4-5% yields. The trade-off is additional regulatory complexity. These instruments look more like securities, requiring compliance structures that pure stablecoins avoid.

Comparison of Stability Mechanisms

| Type | Examples | Backing Asset | Stability Rating | Capital Efficiency | Decentralization | Best Suited For |

|---|---|---|---|---|---|---|

| Fiat-Collateralized | USDT, USDC | Real dollars, T-bills | High | High (1:1) | Low | Trading, payments, institutional use |

| Crypto-Collateralized | DAI, MIM | Over-collateralized crypto | Moderate-High | Low (150-200%) | High | DeFi lending, decentralized applications |

| Algorithmic | UST (failed), FRAX* | Supply algorithms ± partial backing | Very Low to Moderate | Very High | High | Experimental (high risk) |

| Delta-Neutral Synthetic | USDe, suiUSDe | Digital assets + short futures | High | High (1:1) | Moderate | Yield-seeking users accepting complexity |

| Treasury Yield-Bearing | USDY, USYC | U.S. Treasuries | High | High (1:1) | Low | Conservative yield seekers |

*Post-Terra, Frax governance voted to increase collateralization toward 100% USDC backing. By 2024, FRAX maintained over 90% collateral backing, effectively operating as a collateralized stablecoin rather than a purely algorithmic one.

What Drives Issuer Design Choices

Why does Circle choose centralized control while MakerDAO prioritizes decentralization? Why does Ethena pursue delta-neutral complexity? The answer involves regulatory environment, target audience, chain selection, and lessons from $60+ billion in historical failures.

Regulatory Pressure Shapes Architecture

Stablecoins exist in regulatory gray areas that are rapidly clarifying. U.S. regulators increasingly treat fiat-backed stablecoins as payment systems requiring licenses, reserves segregation, and compliance infrastructure. This regulatory reality makes centralization not just acceptable but required for certain issuers.

Circle operates as a licensed money transmitter in most U.S. states. This licensing enables banking relationships that hold reserves. The price is complete regulatory oversight: know-your-customer requirements, transaction monitoring, sanctions compliance, and the ability to freeze addresses. Circle accepts these requirements to operate legally and attract institutional users.

Projects prioritizing regulatory avoidance choose crypto-backed or algorithmic models. Operating through smart contracts rather than companies creates distance from existing financial regulations. This enables permissionless access but excludes regulated institutions.

The regulatory landscape keeps evolving. Europe's MiCA regulation, implemented in 2024, creates clear stablecoin rules. The U.S. moves toward comprehensive stablecoin legislation. These developments favor designs that can comply.

Target Audience Determines Priorities

Retail traders value simplicity and stability. They need stablecoins that work reliably across exchanges, maintain tight pegs, and enable fast trading. USDT dominates because it offers deep liquidity on every major exchange globally. Traders don't care about decentralization. They care about execution speed and peg reliability.

DeFi protocols need composability and permissionless access. DAI integrates seamlessly with Aave, Compound, Uniswap, and hundreds of other protocols. No permission needed, no accounts to create, no compliance checks. This composability makes DAI the DeFi standard despite lower capital efficiency.

Institutions prioritize regulatory compliance and transparent reserves. USDC wins institutional adoption because Circle provides audit reports, maintains regulated banking, and cooperates with authorities. Banks exploring blockchain payments choose USDC. Corporations holding crypto treasury reserves choose USDC. Compliance infrastructure matters more than perfect decentralization.

Chain Environment Influences Design

Ethereum's high costs favor capital-efficient designs. Deploying complex smart contracts and executing frequent liquidations gets expensive at $50 per transaction. Fiat-backed models minimize on-chain complexity: simple minting and burning rather than intricate collateral management.

Layer 2 networks and alternative Layer 1s enable more complex mechanisms. Arbitrum's lower fees make crypto-backed models more viable. Solana's speed enables sophisticated algorithmic experiments. Base's growing ecosystem attracts new stablecoin designs.

Cross-chain requirements increasingly matter. Users want stablecoins that work across Ethereum, Solana, Base, Arbitrum, and other networks. Fiat-backed models handle this through wrapped versions controlled by the issuer. Crypto-backed models face greater technical challenges maintaining consistent collateral across chains.

Historical Failures Inform Current Designs

Terra's $60 billion collapse taught specific lessons that shape current development:

- Pure algorithmic mechanisms fail catastrophically. Partial backing provides necessary stability cushions.

- Death spirals accelerate in both directions. Systems need circuit breakers and backstops.

- Confidence matters more than code. Transparency and proof of reserves build trust that mechanism design alone cannot create.

- Stress testing against extreme scenarios is mandatory. Designs that work in stable markets often break during volatility.

Every major stablecoin project now studies what went wrong with UST. Even algorithmic advocates like Frax added significant USDC backing to prevent similar failures. The lessons are painful but clear.

| Fiat-Backed | Crypto-Backed | Algorithmic | Delta-Neutral | Yield-Bearing | |

|---|---|---|---|---|---|

| Regulatory stance | Compliance-first | Avoidance | Avoidance | Hybrid | Compliance-adjacent |

| Primary audience | Institutions, traders | DeFi protocols | Speculators | Yield seekers | Conservative yield |

| Chain preference | Any (simple contracts) | L2s (low-fee liquidations) | High-speed L1s | Multi-chain | Any |

| Key risk | Custodial / freeze | Liquidation cascade | Death spiral | Funding rate flip | Regulatory reclassification |

Understanding these mechanism families and their trade-offs provides the foundation for evaluating any stablecoin. The technical choices matter less than the trade-offs they represent. When examining a new stablecoin, ask: How does it handle the trilemma? What breaks under stress? Who controls the system? The answers reveal whether the design can deliver on its promises.

- Every stablecoin sacrifices one trilemma corner: USDC accepts centralization, DAI accepts capital inefficiency, and Terra surrendered stability itself.

- TerraUSD grew to $18 billion in circulation, then collapsed in 72 hours, wiping out $60 billion total once the confidence sustaining it disappeared.

- USDT and USDC together control over 90% of the $300 billion stablecoin market because most users choose reliable stability over decentralization.

- Circle earns roughly $2.5 billion annually keeping USDC reserve yields, but yield-bearing models like USDY redistribute that income to token holders instead.

- USDe reached $14 billion by collecting 5-15% funding rates from delta-neutral futures positions, earning yield without algorithmic risk or overcollateralization.